UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended December 31, 2010

OR

|

¨

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from to

Commission File Number 001-06605

EQUIFAX INC.

(Exact name of registrant as specified in its charter)

|

Georgia

|

58-0401110

|

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

|

1550 Peachtree Street, N.W.

Atlanta, Georgia

|

30309

|

|

(Address of principal executive offices)

|

(Zip Code)

|

Registrant’s telephone number, including area code: 404-885-8000

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

Name of each exchange on which registered

|

|

Common Stock, $1.25 par value per share

|

|

New York Stock Exchange

|

|

Common Stock Purchase Rights

|

|

New York Stock Exchange

|

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Exchange Act (“Act”). x YES ¨ NO

Indicate by check mark if Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ¨ YES x NO

Indicate by check mark whether Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x YES ¨ NO

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). YES x NO ¨

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

x Large accelerated filer

|

¨ Accelerated filer

|

¨ Non-accelerated filer

|

¨ Smaller reporting company

|

| |

(Do not check if a smaller reporting company)

|

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Act).¨ YES x NO

As of June 30, 2010, the aggregate market value of Registrant’s common stock held by non-affiliates of Registrant was approximately $3,507,932,713 based on the closing sale price as reported on the New York Stock Exchange. At January 31, 2011, there were 122,739,885 shares of Registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of Registrant’s definitive proxy statement for its 2011 annual meeting of shareholders are incorporated by reference in Part III of this 10-K.

PART I

ITEM 1. BUSINESS

OVERVIEW

Equifax Inc. is a leading global provider of information solutions for businesses and consumers. We have a large and diversified group of clients and customers, including financial institutions, corporations, governments and individuals. Our products and services are based on comprehensive databases of consumer and business information derived from numerous types of credit, financial, employment and income, public record, demographic and marketing data. We use proprietary analytical tools to analyze this data to create customized insights, decision-making solutions and processing services for businesses. We help consumers understand, manage and protect their personal information and make more informed financial

decisions. Additionally, we are a leading provider of payroll-related and human resources business process outsourcing services in the United States of America, or U.S.

We currently operate in three global regions: North America (U.S. and Canada), Europe (the United Kingdom, or U.K., Spain and Portugal) and Latin America (Argentina, Brazil, Chile, Ecuador, El Salvador, Honduras, Paraguay, Peru and Uruguay). We also maintain support operations in Costa Rica and the Republic of Ireland. We own an equity interest in a consumer credit information company in Russia. During 2009, we formed a joint venture to provide a broad range of credit data and information solutions in India. Of the countries in which we operate, 73% of our revenue was generated in the U.S. during 2010.

Equifax was originally incorporated under the laws of the State of Georgia in 1913, and its predecessor company dates back to 1899. As used herein, the terms Equifax, the Company, we, our and us refer to Equifax Inc., a Georgia corporation, and its consolidated subsidiaries as a combined entity, except where it is clear that the terms mean only Equifax Inc.

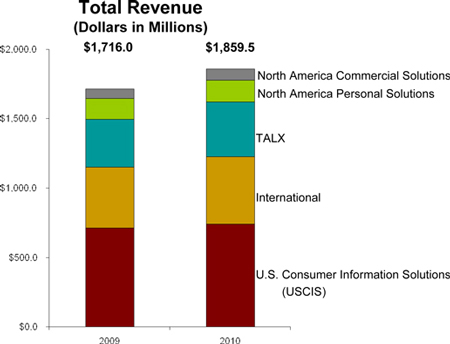

We are organized and report our business results in five operating segments, as follows:

|

|

•

|

U.S. Consumer Information Solutions (USCIS) — provides consumer information solutions to businesses in the U.S. including online credit data and credit decision technology solutions (OCIS), mortgage reporting and settlement solutions, and consumer financial marketing services (CFMS).

|

|

|

•

|

International — includes our Canada Consumer, Europe and Latin America business units. Products and services offered are similar to those available in the USCIS, North America Commercial Solutions and North America Personal Solutions operating segments but vary by geographic region.

|

|

|

•

|

TALX — provides services enabling clients to outsource and automate the performance of certain payroll-related and human resources business processes, including employment, income and social security number verification, employment-related tax management and talent management services.

|

|

|

•

|

North America Personal Solutions — provides products to consumers enabling them to monitor, manage and protect their credit, credit score and identity information and make more informed financial decisions.

|

|

|

•

|

North America Commercial Solutions — provides credit, financial, marketing and other information regarding businesses in the U.S. and Canada.

|

Our revenue base and business mix are diversified among our five segments as depicted in the chart below.

PRODUCTS AND SERVICES

The following chart summarizes the key products and services offered by each of the business units within our segments:

| |

|

USCIS

|

|

North

|

|

North

|

|

International

|

|

TALX

|

|

| |

|

OCIS

|

|

CFMS

|

|

Mortgage

Services

|

|

America

Personal

Solutions

|

|

America

Commercial

Solutions

|

|

Canada

Consumer

|

|

Europe

|

|

Latin

America

|

|

The Work

Number ®

|

|

Tax & Talent

Management

Services

|

|

|

Online consumer credit reports

|

|

X

|

|

|

|

X

|

|

X

|

|

|

|

X

|

|

X

|

|

X

|

|

|

|

|

|

|

Consumer alerts, scores and analytical services

|

|

X

|

|

X

|

|

X

|

|

X

|

|

|

|

X

|

|

X

|

|

X

|

|

X

|

|

|

|

|

Enabling technology services (i.e., credit decisioning platforms)

|

|

X

|

|

|

|

X

|

|

|

|

X

|

|

X

|

|

X

|

|

X

|

|

|

|

|

|

|

Identity authentication/fraud

|

|

X

|

|

|

|

|

|

|

|

X

|

|

X

|

|

X

|

|

X

|

|

X

|

|

|

|

|

Consumer financial marketing services

|

|

|

|

X

|

|

X

|

|

|

|

|

|

X

|

|

X

|

|

X

|

|

|

|

|

|

|

Business credit reports, scores and analytical services

|

|

|

|

|

|

|

|

|

|

X

|

|

|

|

X

|

|

X

|

|

|

|

|

|

|

Business marketing services and database management

|

|

|

|

|

|

|

|

|

|

X

|

|

|

|

X

|

|

X

|

|

|

|

|

|

|

Business demographic information

|

|

|

|

|

|

|

|

|

|

X

|

|

|

|

X

|

|

|

|

|

|

|

|

|

Direct to consumer credit monitoring

|

|

|

|

|

|

|

|

X

|

|

|

|

|

|

X

|

|

|

|

|

|

|

|

|

Identity protection

|

|

|

|

|

|

|

|

X

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Debt Reduction Solutions

|

|

|

|

|

|

|

|

X

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Employment, income and identity verification services

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

X

|

|

|

|

|

Business Process Outsourcing (BPO)

|

|

|

|

|

|

X

|

|

|

|

|

|

|

|

|

|

|

|

X

|

|

X

|

|

Each of our operating segments is described more fully below.

USCIS

USCIS provides consumer information solutions to businesses in the U.S. through three product lines, as follows:

Online Consumer Information Solutions (OCIS). OCIS products are derived from large databases of credit information that we maintain about individual consumers, including credit history, current credit status and consumer address information. Our customers utilize the credit report information we provide to make decisions for a wide range of credit and business purposes, such as whether, and on what terms, to approve auto loans or credit card applications, whether to allow a consumer to open a new utility or telephone account and similar business uses. We offer other data, analytical and predictive services based on the information in the

consumer credit information databases to help further mitigate the risk of granting credit by verifying the identity of a consumer seeking credit, predicting the risk of consumer bankruptcy, or indicating the credit applicant’s risk potential for account delinquency, for example. These risk management services, as well as fraud detection and prevention services, enable our customers to monitor default rates and proactively manage their existing credit card or other consumer loan accounts, and ensure a consumer’s identity.

OCIS customers access products through a full range of electronic distribution mechanisms, including direct real-time access, which facilitates instant decisions, such as the immediate granting of credit at the point of sale. We also develop and host customized applications that enhance the decision-making process for our customers. These decisioning technology applications assist with pre-approved offers of credit, cross-selling of various banking products, determining deposit amounts for telephone and utility companies, and verifying the identity of consumer customers.

Mortgage Solutions. Our Mortgage Solutions products, offered in the U.S., consist of specialized credit reports that combine the reports of the three major consumer credit reporting agencies (Equifax, Experian Group and TransUnion LLC) into a single credit report provided in an online format, commonly referred to as a tri-merge report. Mortgage lenders use these tri-merge reports in making their mortgage underwriting decisions. We also offer certain mortgage settlement services, such as appraisal, title and closing services, with our traditional mortgage service offerings, with certain of these services provided through agreements with third

parties.

Consumer Financial Marketing Services (CFMS). Our CFMS products apply consumer financial information to enable our customers to manage their marketing efforts, including targeting and segmentation, for efficiency and effectiveness; identify and acquire new customers for their financial products and services; and realize additional revenue from existing customers. These products utilize information derived from actual consumer data, including credit, income, asset, liquidity, net worth and spending activity, which also support many of our OCIS products. These data assets broaden the understanding of customer financial potential and

opportunity which can further drive breakthrough decisioning and targeting solutions for our customers. We also provide account review services which assist our customers in managing their existing customers and prescreen services that help our clients identify potential new customers. Customers for these products primarily include institutions in the banking, brokerage, insurance, and mortgage industries as well as companies primarily focused on digital and interactive marketing.

International

The International operating segment includes our Canada Consumer, Europe and Latin America business units. These business units offer products that are similar to those available in the USCIS operating segment, although data sources tend to rely more heavily on government agencies than in the U.S. These products generate revenue in Argentina, Brazil, Canada, Chile, Ecuador, El Salvador, Honduras, Paraguay, Peru, Portugal, Spain, the U.K. and Uruguay. We also maintain support operations in the Republic of Ireland and Costa Rica. We offer consumer credit services in Russia and India through joint ventures.

Canada Consumer. Similar to our OCIS, Mortgage Solutions and CFMS business units, Canada Consumer offers products derived from the credit information that we maintain about individual consumers. We offer many products in Canada, including credit reporting and scoring, consumer marketing, risk management, fraud detection and modeling services, together with certain of our decisioning products that facilitate pre-approved offers of credit and automate a variety of credit decisions.

Europe. Our European operation provides information solutions, marketing and personal solutions products. Information solutions and personal solutions products are generated from credit records that we maintain and include credit reporting and scoring, risk management, fraud detection and modeling services. Both of these products are sold in the U.K. and our information solutions products are sold in Portugal and Spain. Our commercial products, such as business credit reporting and commercial risk management services, are only available in the U.K. Marketing products, which are similar to those offered in our CFMS business unit, are

primarily available in the U.K. and, to a lesser extent, in Spain.

Latin America. Our Latin American operation provides consumer and commercial information solutions products and marketing products. We offer a full range of consumer products, generated from credit records that we maintain, including credit reporting and scoring, risk management, identity verification and fraud detection services. Our consumer products are the primary source of revenue in each of the countries in which we operate, with the exception of Brazil where the majority of our revenue comes from commercial products. We offer our commercial products, which include credit reporting, decisioning tools and risk management services, in

varying degrees to the countries we serve. We also provide a variety of consumer and commercial marketing products generated from our credit information databases, including business profile analysis, business prospect lists and database management, in varying degrees in the countries we serve. The other countries in which we operate include Argentina, Chile, Ecuador, El Salvador, Honduras, Paraguay, Peru and Uruguay.

TALX

TALX operates in the U.S. through two business units, as follows:

The Work Number® (TWN Services). TWN Services include employment, income and social security number verification services and complementary services which include W-2 management services (which include initial distribution, reissue and correction of W-2 forms); paperless pay services that enable employees to electronically receive pay statement information as well as review and change direct deposit account or W-4 information; integrated

electronic time capture and reporting services; paperless new-hire services to bring new workers on board using electronic forms; and I-9 management services designed to help clients electronically comply with the immigration laws that require employers to complete an I-9 form for each new hire.

TWN Services enable employers to direct third-party verifiers to our website or to a toll-free telephone number to verify the employee’s employment status and income data. We also offer an offline research verification service which expands employment verification to locate data outside our existing TWN database. In 2009, we increased our services to provide IRS income verifications using the IncomeChek® product as well as identity verification through a secure, web-based portal using the DirectChek® product.

We rely on payroll data received from over 2,400 organizations, including over half of Fortune 500 companies, to regularly update the TWN database. This data is updated as employers transmit data electronically directly to us each payroll period. Employers contract to provide this data to us for specified periods under the terms of contracts which range from one to five years. We use this data to provide employment and income verifications to third-party verifiers; the fees we charge for these services are generally per transaction. After the expiration of the applicable contract, absent renewal by mutual agreement of the parties, we generally do not have any further right to use the employment data we obtained

pursuant to the contract. We have not experienced significant turnover in the employer contributors to the TWN database because we generally do not charge them to add their employment data to the database and the verification service we offer relieves them of the administrative burden and expense of responding to third party employment verification requests. The database contained approximately 220 million current and historic employment records at December 31, 2010.

Tax and Talent Management Services. These services are aimed at reducing the cost to the human resources function of businesses by assisting with employment tax matters and planning and improving the cost-effectiveness of talent recruitment and management. We offer a broad suite of services designed to reduce the cost of unemployment claims through effective claims representation and management and efficient processing and to better manage the tax rate that employers are assessed for unemployment taxes. We also offer our customers comprehensive services designed to research the availability of employment-related tax credits (e.g., the

federal work opportunity and welfare to work tax credits and state tax credits), process the necessary filings and assist the customer in obtaining the tax credit. In talent management, we also offer secure, electronic-based psychometric testing and assessments, as well as onboarding services using online forms to complete the new hire process for employees of corporate and government agencies.

North America Personal Solutions

Our Personal Solutions products give consumers information to make financial decisions and monitor and protect credit, credit score and identity information through our Equifax Complete, ID Patrol, Credit Watch and Score Watch monitoring products. Consumers can obtain a copy of credit file information about them and their credit score. We offer monitoring products for consumers who are concerned about identity theft and data breaches, including the Credit Report Control service that allows consumers subscribing to our credit monitoring products to restrict access to their credit report to mitigate unauthorized use of Equifax credit file information by third parties. Our Debt Wise product utilizes credit report

information to assist consumers in creating a debt repayment plan. Our products are available to consumers directly and through relationships with business partners who distribute our products or provide these services to their employees or customers.

North America Commercial Solutions

Our Commercial Solutions products are derived from databases of credit, financial and marketing information regarding businesses in the U.S. and Canada. The business records included in the U.S. credit database have been developed in part from the Small Business Financial Exchange, Inc., or SBFE. SBFE members, including a number of commercial lending financial institutions, contribute their data to the member-owned SBFE database which we exclusively manage. Our contract with the SBFE to manage this database is scheduled to expire in 2012, unless renewed by mutual agreement of the parties. The information comprising the database is generally not owned by us, and the participating organizations could discontinue

contributing information to the database or our management contract may not be renewed; however, we believe that such an event is unlikely because contributors to the database use the aggregated information in the database to conduct their business and we have a good working relationship with the SBFE members as one of the original founders of this database.

Other databases we have compiled include loan; credit card; public records and leasing history data; trade accounts receivable performance; and Secretary of State and Securities and Exchange Commission registration information. We also offer scoring and analytical services that provide additional information to help mitigate the credit risk assumed by our customers. We also have a marketing database which hosts approximately 47 million commercial demographic data records from around the world helping companies to identify corporate family structures for enterprise visibility of customers and suppliers.

OUR BUSINESS STRATEGY

Our strategic objective is to be the trusted provider of information driven solutions that empower our customers with the ability to make critical decisions with greater confidence. Data is at the core of our value proposition. Leveraging our extensive resources, we deliver differentiated decisions through advanced data, analytics and technology. Our comprehensive set of data assets can provide a complete, 360 degree view of the consumer’s financial potential and opportunity including their propensity, ability and capacity to pay. Our long-term corporate growth strategy is driven by the following initiatives:

|

|

•

|

Increase penetration of our customers’ information solutions needs. We seek to increase our share of customers’ spending on information-related services through the development and introduction of new products such as ID management, pricing our services in accordance with the value they create, increasing the range of current services utilized by our customers, and improving the quality of sales and customer support interactions with consumers. We are also helping customers address increasing compliance requirements through the development of new products.

|

|

|

•

|

Deploy decisioning technologies and analytics globally. We continue to invest in and develop new technology to enhance the functionality, cost-effectiveness and security of the services we offer and further differentiate our products from those offered by our competitors. In addition to custom products for large customers, we develop off-the-shelf, decisioning technology platforms that are more cost-effective for medium- and smaller-sized customers. We also develop predictive scores and analytics to help customers acquire new customers and manage their existing customer relationships. We develop a broad array of industry, risk management, cross-sell and account acquisition models to enhance the precision of our customers’

decisioning activities.

|

|

|

•

|

Invest in unique data sources. We continue to invest in and acquire unique sources of credit and non-credit information to enhance the variety and quality of our services while increasing customers’ confidence in information-based business decisions. Areas of focus for investment in new sources of data include, among others, positive payment data, real estate data and new commercial business data. As an example, we acquired IXI Corporation in 2009, which added valuable and unique U.S. consumer data related to employment and financial assets which broadens and enriches the types of services we can offer our customers.

|

|

|

•

|

Pursue new vertical markets and expand into emerging markets. We see numerous opportunities to expand into emerging markets both in the U.S. and internationally. In the U.S., our Capital Markets area offers unique products which enable investors and underwriters to have a more current and relevant understanding of the inherent risk in a portfolio of loans. Our Mortgage Services business continues to expand its presence in the mortgage value chain with a broader offering of mortgage underwriting services. During 2010, we acquired Anakam, Inc. which is a provider of large-scale, software-based, multi-factor authentication solutions. Internationally, we are investing in and building Russian and Indian ventures, as well as our existing served

markets.

|

COMPETITION

The market for our products and services is highly competitive and is subject to constant change. Our competitors vary widely in size and the nature of the products and services they offer. Sources of competition are numerous and include the following:

|

|

•

|

Competition for our consumer information solutions and personal solutions products varies by both application and industry, but generally includes two global consumer credit reporting companies, Experian, and TransUnion, both of which offer a product suite similar to ours, and LifeLock, a national provider of personal identity theft protection products. There are also a large number of smaller competitors who offer competing products in specialized areas (such as fraud prevention, risk management and application processing and decisioning solutions) and software companies offering credit modeling services or analytical tools. We believe that our products offer our customers an advantage over those of our competitors because of the quality of our data files, which we believe to be superior in

terms of depth, accuracy and availability. Other differentiators include our decisioning technology and the capabilities of our analytical services. Our competitive strategy is to emphasize customer solutions and quality while remaining competitive on price. Our marketing services products also compete with the foregoing companies and others who offer demographic information products, including Acxiom Corporation, Harte-Hanks, Inc. and infoGROUP, Inc. We also compete with Fair Isaac Corporation with respect to our analytical tools.

|

|

|

•

|

Competition for our commercial solutions products primarily includes Experian and The Dun & Bradstreet Corporation and providers of these services in the international markets we serve. We believe our U.S. small business loan information from financial institutions creates a unique database and product for the small business segment of that market.

|

|

|

•

|

Competition for our employment and income verification services includes large employers who serve their own needs through in-house systems to manage verification as well as regional online verification companies, such as Verify Jobs and First Advantage, who offer verification services along with other human resources and tax services. Competition for complementary TWN Services includes payroll processors such as Automatic Data Processing, Inc., or ADP, Paychex, Inc. and Ceridian Corporation. Competitors of our Tax Management Services include in-house management of this function primarily by large employers; ADP; and a number of smaller regional firms that offer tax management services (including Barnett Associates, Thomas & Thorngren, UC Advantage). Talent Management Services competitors

include assessment service providers that offer proprietary content (Previsor, Inc., Development Dimensions International, Brainbench, Inc.), human resources consulting firms (AON Corporation, Towers Watson, Right Management Consulting) and assessment or test publishers that have proprietary delivery platforms (Devine Group, Inc., Hogan Assessments Systems, Inc., SHL Group plc).

|

While we believe that none of our competitors offers the same mix of products and services as we do, certain competitors may have larger shares of particular geographic or product markets or operate in geographic areas where we do not currently have a presence.

We assess the principal competitive factors affecting our markets to include: product attributes such as quality, adaptability, scalability, interoperability, functionality and ease-of-use; product price; technical performance; access to unique proprietary databases; availability in application service provider, or ASP, format; quickness of response, flexibility and customer services and support; effectiveness of sales and marketing efforts; existing market penetration; new product innovation; and our reputation as a trusted steward of information.

MARKETS AND CUSTOMERS

Our products and services serve clients across a wide range of industries, including financial services, mortgage, human resources, consumer, commercial, telecommunications, retail, automotive, utilities, brokerage, healthcare and insurance industries, as well as state and federal governments. We also serve consumers directly. Our revenue stream is highly diversified with our largest customer providing only 3% of total revenue. The following table summarizes the various end-user markets we serve:

| |

|

Percentage of

Consolidated Revenue

|

|

| |

|

2010

|

|

|

2009

|

|

|

Financial

|

|

|

26 |

% |

|

|

26 |

% |

|

Mortgage

|

|

|

15 |

% |

|

|

14 |

% |

|

Employers

|

|

|

11 |

% |

|

|

10 |

% |

|

Consumer

|

|

|

10 |

% |

|

|

10 |

% |

|

Commercial

|

|

|

8 |

% |

|

|

7 |

% |

|

Telecommunications

|

|

|

7 |

% |

|

|

6 |

% |

|

Retail

|

|

|

5 |

% |

|

|

5 |

% |

|

Automotive

|

|

|

4 |

% |

|

|

4 |

% |

|

Other (1)

|

|

|

14 |

% |

|

|

18 |

% |

| |

|

|

100 |

% |

|

|

100 |

% |

|

(1)

|

Other includes revenue from marketing services, government, insurance and health care end-users.

|

We market our products and services primarily through our own direct sales organization that is organized around sales teams that focus on customer segments typically aligned by vertical markets and geography. Sales groups are based in our headquarters in Atlanta, Georgia, and field offices located in the U.S. and in the countries where we have operations. We also market our products and services through indirect channels, including alliance partners, joint ventures and other resellers. In addition, we sell through direct mail and various websites, such as www.equifax.com.

Our largest geographic market segments are North America (the U.S. and Canada); Europe (the U.K., Spain and Portugal); and Latin America (Argentina, Brazil, Chile, Ecuador, El Salvador, Honduras, Paraguay, Peru and Uruguay). We also maintain support operations in Costa Rica and the Republic of Ireland. We own an equity interest in a consumer credit information company in Russia. During 2009, we formed a joint venture to provide a broad range of credit data and information solutions in India.

Revenue from international customers, including end-users and resellers, amounted to 27% of our total revenue in 2010 and 2009 and 29% of our total revenue in 2008.

TECHNOLOGY AND INTELLECTUAL PROPERTY

We generally seek protection under federal, state and foreign laws for strategic or financially important intellectual property developed in connection with our business. Certain intellectual property, where appropriate, is protected by registration under applicable trademark laws or by prosecution of patent applications. We own several patents registered in the U.S. and certain foreign countries. We also have certain registered trademarks in the U.S. and in many foreign countries. The most important of these are “Equifax,” “TALX”, “The Work Number” and many variations thereof. These trademarks are used in connection with most of our product lines and services. Although these

patents and trademarks are important and valuable assets in the aggregate, no single patent, group of patents or trademark, other than our Equifax trademark, is critical to the success of our business.

We license other companies to use certain data, technology and other intellectual property rights we own or control, primarily as core components of our products and services, on terms that are consistent with customary industry standards and that are designed to protect our interest in our intellectual property.

We are licensed by others to use certain data, technology and other intellectual property rights they own or control, none of which is material to our business except for a license from Fair Isaac Corporation, relating to certain credit-scoring algorithms and the right to sell credit scores derived from them. This license has a five-year term expiring in June 2013 and provides for usage-based fees. Additionally, the licenses do not contain early termination provisions except for standard provisions providing the right to terminate in the event of breach by the other party. We do not hold any franchises or concessions that are material to our business or results of operations.

INFORMATION SECURITY AND GOVERNMENT REGULATION

Safeguarding the privacy and security of consumer credit information, whether delivered online or in an offline format, is a top priority. We recognize the importance of secure online transactions and we maintain physical, administrative, and technical safeguards to protect personal and business identifiable information. We have security protocols and measures in place to protect information from unauthorized access or alteration. These measures include internal and external firewalls, physical security and technological security measures, and encryption of certain data.

Our databases are regularly updated by information provided by financial institutions, telecommunications companies, other trade credit providers, employers, public records vendors and government agencies. Various laws and regulations govern the collection and use of this information. These laws and regulations impact how we are able to provide information to our customers and have significantly increased our compliance costs. We are subject to differing laws and regulations depending on where we operate.

U.S. Data and Privacy Protection

Our U.S. operations are subject to various federal and state laws and regulations governing the collection, protection and use of consumer credit and other information, and imposing sanctions for the misuse of such information or unauthorized access to data. Many of these provisions also affect our customers’ use of consumer credit or other data we furnish. The information underlying our North America Commercial Services business is less regulated than the other portions of our business.

These laws and regulations that may apply to portions of our business include, but are not limited to, the following:

|

|

•

|

The Fair Credit Reporting Act, or FCRA, which governs among other things the reporting of information to consumer reporting agencies that engage in the practice of assembling or evaluating certain information relating to consumers, including our credit reporting business and employment verification; making prescreened offers of credit; the sharing of consumer report information among affiliated and unaffiliated third parties; access to credit scores; and requirements for data furnishers and users of consumer report information. Violation of the FCRA, or of similar state laws, can result in an award of actual damages, as well as statutory and/or punitive damages in the event of a willful violation.

|

|

|

•

|

The Fair and Accurate Credit Transactions Act of 2003, or FACT Act, which amended the FCRA and requires, among other things, nationwide consumer credit reporting agencies, such as us, upon the request of a consumer, to place a fraud alert in the consumer’s credit file stating that the consumer may be the victim of identity theft or other fraud, and furnish a free annual credit file disclosure to consumers through a centralized request facility we have established with the other nationwide credit reporting agencies. FACT Act regulations also require financial institutions to develop policies and procedures to identify potential identity theft, and consumer credit report notice requirements for lenders that use consumer report information in connection with risk-based credit pricing

actions. Entities that furnish information to consumer reporting agencies are required to implement procedures and policies regarding the accuracy and integrity of the furnished information and regarding the correction of previously furnished information that is later determined to be inaccurate. Mortgage lenders are required to disclose credit scores to consumers. Additionally, the FACT Act prohibits a business that receives consumer information from an affiliate from using that information for marketing purposes unless the consumer is first provided a notice and an opportunity to direct the business not to use the information for such marketing purposes (“opt-out”), subject to certain exceptions.

|

|

|

•

|

The Financial Services Modernization Act of 1999, or Gramm-Leach-Bliley Act, or GLB, which, among other things, regulates the use of non-public personal financial information of consumers that is held by financial institutions. Equifax is subject to various GLB provisions, including rules relating to the physical, administrative and technological protection of non-public personal financial information. Breach of the GLB can result in civil and/or criminal liability and sanctions by regulatory authorities, such as fines of up to $100,000 per violation and up to five years imprisonment for individuals.

|

|

|

•

|

The Health Insurance Portability and Accountability Act of 1996, or HIPAA, which requires reasonable safeguards to prevent intentional or unintentional use or disclosure of protected health information.

|

|

|

•

|

Federal and state laws governing the use of the Internet and regulating telemarketing, including the federal Controlling the Assault of Non-Solicited Pornography and Marketing Act of 2003, or CAN-SPAM, which regulates commercial email, prohibits false or misleading header information, requires that a commercial email be identified as an advertisement, and requires that commercial emails give recipients an opt-out method. Senate Bill 3386, signed into federal law on December 29, 2010, seeks to protect online consumers from unfair and deceptive sales tactics on the Internet. Other Internet privacy laws and regulations have been proposed from time to time to address digital marketing, i.e., how personal information is collected and distributed online, including behavioral advertising.

|

|

|

•

|

Fannie Mae and Freddie Mac regulations applicable to our credit reporting and mortgage solutions products, the Real Estate Settlement Procedures Act and HUD’s Regulation X, which requires the disclosure of certain basic information to borrowers concerning settlement costs and prohibits the charging of unearned fees and certain “kickbacks” or other fees for referrals in connection with a residential mortgage settlement service.

|

On July 21, 2010, the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act) became law. The Dodd-Frank Act represents a comprehensive overhaul of the financial services industry within the U.S., establishes the new Bureau of Consumer Financial Protection (the "BCFP") within the Federal Reserve Board, and will require the BCFP and other federal agencies to implement many new and significant rules and regulations. The BCFP will have sweeping powers to administer and enforce a new federal regulatory framework of consumer financial regulation. The Dodd-Frank Act will allow consumers free access to their credit score if their score negatively affects

them in a financial transaction or a hiring decision, and also gives consumers access to credit score disclosures as part of an adverse action and risk-based pricing notice. At this time, it is difficult to predict the extent to which the Dodd-Frank Act or the resulting rules and regulations will impact the U.S. economy or our business. Compliance with these new laws and regulations may require changes in the way we conduct our business and may result in additional compliance costs, which could be significant and could adversely impact our results of operations, financial condition or liquidity.

A number of states in the U.S. have passed versions of security breach notification and credit file freeze legislation. A file freeze enables consumers to place and lift a freeze on access to their credit files. File freeze laws impose differing requirements on credit reporting agencies with respect to how and when to respond to such credit file freeze requests and in the fees, if any, the agencies may charge for freeze-related actions.

International Data and Privacy Protection

We are subject to data protection, privacy and consumer credit laws and regulations in the foreign countries where we do business.

|

|

•

|

In Canada, the Personal Information Protection and Electronic Documents Act (2000) applies to organizations with respect to personal information that they collect, use or disclose in the course of commercial activities. It requires compliance with the National Standard of Canada Model Code for the Protection of Personal Information, covering accountability and identifying purposes, consent, collection, use, disclosure, retention, accuracy, safeguards, individual access and compliance. The Federal Privacy Commissioner is invested with powers of investigation and intervention, and provisions of Canadian law regarding civil liability apply in the event of unlawful processing which is prejudicial to the persons concerned.

|

|

|

•

|

In Europe, Equifax is subject to the European Union, or EU, data protection laws, including the comprehensive EU Directive on Data Protection (1995), which imposes a number of obligations on Equifax with respect to use of personal data, and includes a prohibition on the transfer of personal information from the EU to other countries that do not provide consumers with an “adequate” level of privacy or security. The EU standard for adequacy is generally stricter and more comprehensive than that of the U.S. and most other countries. In the U.K., in addition to the EU Directive on Data Protection, the Data Protection Act of 1998 regulates the manner in which we can use third-party data. In addition, regulatory limitations affect our use of the Electoral Roll, one of our key data

sources in the U.K. Generally, the data underlying the products offered by our U.K. Information Services and Personal Solutions product lines, excluding our Commercial Services products, are subject to these regulations. In Spain and Portugal, the privacy laws which are subject to the EU Directive on Data Protection regulate all credit bureau and personal solutions activities. Except for negative data, the laws in Spain and Portugal generally require consumer consent for all Equifax activities.

|

|

|

•

|

In Latin America, consumer data protection and privacy laws and regulations exist in Argentina, Chile, Peru and Uruguay. Uruguay generally follows the EU data protection model. There are also constitutional provisions in Argentina, Brazil, Chile, Peru and certain other countries which declare the right to seek judicial protection regarding the use of personal data, and in many of those countries grant individuals the right to access and correction of information in the possession of data controllers.

|

Tax Management Services

The Tax Management business within our TALX segment is potentially impacted by changes in U.S. tax laws or interpretations, for example, those pertaining to work opportunity tax credits and unemployment compensation claims. A subsidiary of TALX, Talent Management, provides employee testing, assessment and talent management services to the federal government through a number of primary contracts and subcontracts with federal agencies, including the Transportation Security Administration. These contracts may be adversely affected by changes in U.S. federal government programs or contractor requirements, including the adoption of new laws or regulations.

Environmental Regulation

We are subject to federal, state and local laws and regulations in the areas of safety, health and environmental protection. Compliance with these laws and regulations has not in the past had any material effect on our earnings, capital expenditures or competitive position. However, the effect of such compliance in the future cannot be predicted. We believe that we are in material compliance with applicable federal, state and local safety, health and environmental regulations.

PERSONNEL

Equifax employed approximately 6,500 employees in 16 countries as of December 31, 2010. None of our U.S. employees are subject to a collective bargaining agreement and no work stoppages have been experienced. Pursuant to local laws, certain of our employees in Argentina, Brazil and Spain are covered under government-mandated collective bargaining regulations that govern general salary and compensation matters, basic benefits and hours of work.

EXECUTIVE OFFICERS OF EQUIFAX

The executive officers of Equifax and their ages and titles are set forth below. Business experience and other information is provided in accordance with SEC rules.

Richard F. Smith (51) has been Chairman and Chief Executive Officer since December 15, 2005. He was named Chairman-Elect and Chief Executive Officer effective September 19, 2005 and was elected as a Director on September 22, 2005. Prior to that, Mr. Smith served as Chief Operating Officer, GE Insurance Solutions, from 2004 to September 2005 and President and Chief Executive Officer of GE Property and Casualty Reinsurance from 2003 to 2004.

Lee Adrean (59) has been Corporate Vice President and Chief Financial Officer since October 2006. Prior to joining Equifax, he served as Executive Vice President and Chief Financial Officer of NDCHealth Corporation from 2004 to 2006. Prior thereto, he served as Executive Vice President and Chief Financial Officer of EarthLink, Inc. from 2000 until 2004.

Kent E. Mast (67) has served as Corporate Vice President and Chief Legal Officer since 2000. His responsibilities include legal services, global sourcing, security and compliance, government and legislative relations, corporate governance and privacy functions.

Coretha M. Rushing (54) has been Corporate Vice President and Chief Human Resources Officer since 2006. Prior to joining Equifax, she served as an executive coach and HR Consultant with Atlanta-based Cameron Wesley LLC. Prior thereto, she was Senior Vice President of Human Resources at The Coca-Cola Company, where she was employed from 1996 until 2004.

Paul J. Springman (65) has served as Corporate Vice President and Chief Marketing Officer since February 2004. Prior thereto, he was head of the Predictive Sciences unit from August 2002 until February 2004.

David C. Webb (55) became Chief Information Officer on January 19, 2010. Prior thereto, he served as Chief Operations Officer for SVB Financial Corp. from 2008, and from 2004 to 2008 was Chief Information Officer. Mr. Webb was Vice President, Investment Banking Division at Goldman Sachs, a leading global investment banking, securities and investment management firm, from 1999 to 2004. He was Chief Information Officer at Bank One from 1997 to 1999.

Rodolfo M. Ploder (50) has been President, U.S. Consumer Information Solutions since July 2010. Prior thereto, he served as President, International from January 2007 until June 2010. Prior thereto, he was Group Executive, Latin America from February 2004 to January 2007.

J. Dann Adams (53) has been President of Equifax’s TALX subsidiary since July 2010. Prior thereto, he served as President, U.S. Consumer Information Solutions from 2007 to June 2010. Prior thereto, he served as Group Executive, North America Information Services from November 2003 until December 2006.

Paulino R. Barros (54) has been President, International since July 2010. Prior thereto, he served as President of PB&C Global Investments, LLC, an international consulting and investment firm. Prior thereto, he was President of Global Operations for AT&T.

Joseph M. Loughran, III (43) has been President, North America Personal Solutions since January 4, 2010. Prior thereto, he was Senior Vice President — Corporate Development from April 2006 to December 2009. Prior to joining Equifax he held various executive roles at BellSouth Corporation from May 2001 to April 2006, including most recently Managing Director-Corporate Strategy and Planning from May 2005 to April 2006. Prior to joining BellSouth, Mr. Loughran held various roles with McKinsey & Company, King & Spalding, and Lazard Frères & Co.

Alejandro (“Alex”) Gonzalez (41) has been President, North America Commercial Solutions since January 4, 2010. Prior thereto, he was Senior Vice President of Strategic Marketing from January 2006 to December 2009, and Customer Experience Leader for GE Insurance Solutions from January 2005 to December 2005.

Nuala M. King (57) has been Senior Vice President and Controller since May 2006. Prior thereto, she was Vice President and Corporate Controller from March 2004 to April 2006. Prior to joining Equifax, Ms. King served as Corporate Controller for UPS Capital from March 2001 until March 2004.

FORWARD-LOOKING STATEMENTS

This report contains information that may constitute “forward-looking statements.” Generally, the words “believe,” “expect,” “intend,” “estimate,” “anticipate,” “project,” “will” and similar expressions identify forward-looking statements, which generally are not historical in nature. All statements that address operating performance, events or developments that we expect or anticipate will occur in the future are forward-looking statements. Management believes that these forward-looking statements are reasonable as and when made. However, forward-looking statements are subject to certain risks and uncertainties that

could cause actual results to differ materially from our Company’s historical experience and our present expectations or projections. These risks and uncertainties include, but are not limited to, those described below in Item 1A. Risk Factors, and elsewhere in this report and those described from time to time in our future reports filed with the United States Securities and Exchange Commission, or SEC. As a result of such risks and uncertainties, we urge you not to place undue reliance on any such forward-looking statements. Forward-looking statements speak only as of the date when made. We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

AVAILABLE INFORMATION

Detailed information about us is contained in our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements and other reports, and amendments to those reports, that we file with, or furnish to, the SEC. These reports are available free of charge at our website, www.equifax.com, as soon as reasonably practicable after we electronically file such reports with or furnish such reports to the SEC. However, our website and any contents thereof should not be considered to be incorporated by reference into this document. We will furnish copies of such reports free of charge upon written request to Corporate Secretary, Equifax Inc., P.O. Box 4081, Atlanta, Georgia,

30302.

ITEM 1A. RISK FACTORS

Our business faces a variety of risks and uncertainties, including those described below, and may include additional risks and uncertainties not presently known to us or that we currently deem immaterial. If any of the events or circumstances described below occurs, our business, financial results or results of operations may be adversely impacted. These risk factors should be read in conjunction with the other information in this Form 10-K.

Weakness in consumer lending activity could materially adversely affect us.

Business customers use our credit information and related analytical services and data to process applications for new credit cards, automobile loans, home and equity loans and other consumer loans, and to manage their existing credit relationships. Bank and other lenders’ willingness to extend credit is adversely affected by elevated consumer delinquency and loan losses in a weak economy. Consumer demand for credit (i.e., rates of spending and levels of indebtedness) also tends to grow more slowly or decline during periods of economic contraction or slow economic growth. High or rising rates of unemployment and interest, declines in income, home prices, or investment values, lower consumer confidence and

reduced access to credit adversely affect demand for our products and services, and consequently our revenue, as consumers may continue to postpone or reduce their spending and use of credit, and lenders may reduce the amount of credit offered or available.

The loss of access to credit and other data from external sources could harm our ability to provide our products and services.

We rely extensively upon data from external sources to maintain our proprietary and non-proprietary databases, including data received from customers, strategic partners and various government and public record sources. This includes the widespread and voluntary contribution of credit data from most lenders in the U.S and many other markets as well as the contribution of data under proprietary contractual agreements, such as employers’ contribution of employment and income data to The Work Number, financial institutions’ contribution of individual financial data to IXI, and financial institutions’ contribution of small business

borrowing information to the Small Business Financial Exchange. Our data sources could withdraw their data from us for a variety of reasons, including legislatively or judicially imposed restrictions on use. We also compete with several of our third-party data suppliers. If a substantial number of data sources or certain key data sources were to withdraw or be unable to provide their data, if we were to lose access to data due to government regulation, or if the collection of data becomes uneconomical, our ability to provide products and services to our clients could be materially adversely impacted, which could result in decreased revenue, net income and earnings per share.

Our markets are highly competitive and new product introductions and pricing strategies being offered by our competitors could decrease our sales and market share or require us to reduce our prices in a manner that reduces our operating margins.

We operate in a number of geographic, product and service markets that are highly competitive. Competitors may develop products and services that are superior to or that achieve greater market acceptance than our products and services. The size of our competitors varies across market segments, as do the resources we have allocated to the segments we target. Therefore, some of our competitors may have significantly greater financial, technical, marketing or other resources than we do in one or more of our market segments, or overall, as is the case in Brazil and the U.K., markets where we face a larger competitor. As a result, our competitors may be in a position to respond more quickly than we can to new or emerging

technologies and changes in customer requirements, or may devote greater resources than we can to the development, promotion, sale and support of products and services. Moreover, new competitors or alliances among our competitors may emerge and potentially reduce our market share, revenue or margins.

Some of our competitors may choose to sell products competitive to ours at lower prices by accepting lower margins and profitability, or may be able to sell products competitive to ours at lower prices given proprietary ownership of data, technological superiority or economies of scale. Price reductions by our competitors could negatively impact our margins and results of operations and could also harm our ability to obtain new customers on favorable terms. Historically, certain of our key products have experienced declines in per unit pricing due to competitive factors and customer demand. Since a significant portion of our operating expenses is relatively fixed in nature due to sales, information technology and

development and other costs, if we were unable to respond quickly enough to changes in competition or customer demand, we could experience further reductions in our operating margins.

If we do not introduce successful new products and services in a timely manner, our products and services will become obsolete and our operating results will suffer.

We generally sell our products in industries that are characterized by rapid technological changes, frequent new product and service introductions and changing industry standards. In addition, certain of the markets in which we operate are seasonal and cyclical. Without the timely introduction of new products, services and enhancements, our products and services will become technologically or commercially obsolete over time, in which case our revenue and operating results would suffer. The success of our new products and services will depend on several factors, including our ability to properly identify customer needs; innovate and develop new technologies, services and applications; successfully commercialize new

technologies in a timely manner; produce and deliver our products in sufficient volumes on time; differentiate our offerings from competitor offerings; price our products competitively; anticipate our competitors’ development of new products, services or technological innovations; and control product quality in our product development process.

The impact of consolidation in the financial services, mortgage, retail, telecommunications and other markets is difficult to predict and may harm our business.

The financial services, mortgage, retail and telecommunications industries are intensely competitive and have been subject to increasing consolidation. Continuation of the consolidation trends in these and other industries could result in lower average prices for the larger combined entities, lower combined purchases of our services than were purchased cumulatively by separate entities prior to consolidation, or existing competitors increasing their market share in newly consolidated entities, which could have a material adverse effect on our business, financial condition and results of operations if we are not retained or chosen as a service provider. We may not be able to compete successfully in an increasingly

consolidated industry and cannot predict with certainty how industry consolidation will affect our competitors or us.

If we are unable to protect our information systems against data corruption, cyber-based attacks or network security breaches, our operations could be disrupted.

We are highly dependent on information technology networks and systems, including the Internet, to process, transmit and store electronic information. In particular, we depend on our information technology infrastructure for business-to-business and business-to-consumer electronic commerce. Security breaches of this infrastructure can create system disruptions, shutdowns or unauthorized disclosure of confidential information. If we are unable to prevent such breaches, our operations could be disrupted, or we may suffer financial damage or loss because of lost or misappropriated information.

Many of our products are accessed through the Internet, including our consumer and commercial information services. Security breaches in connection with the delivery of our products and services via the Internet may affect us or our industry and could be detrimental to our reputation, business, operating results and financial condition. We cannot be certain that advances in criminal capabilities, new discoveries in the field of cryptography or other developments will not compromise or breach the technology protecting the networks that access our products and services.

Dependence on outsourcing certain portions of our supply and distribution chain may adversely affect our ability to bring products to market and damage our reputation. Dependence on outsourced information technology and other administrative functions may impair our ability to operate effectively.

As part of our efforts to streamline operations and to reduce operating costs, we have outsourced various components of our application development, information technology, operational support and administrative functions and will continue to evaluate additional outsourcing. Although we have implemented service level agreements and have established monitoring controls, if our outsourcing vendors fail to perform their obligations in a timely manner or at satisfactory quality levels, our ability to bring products to market and support our customers, and our reputation could suffer. Any failure to perform on the part of these third party providers could impair our ability to operate effectively and could result in

lower future revenue, unexecuted efficiencies and adversely impact our results of operations and our stock price. Much of our outsourcing takes place in developing countries and, as a result, may be subject to geopolitical uncertainty.

If we experience system failures, the delivery of our products and services to our customers could be delayed or interrupted, which could harm our business and reputation and result in the loss of customers.

Our ability to provide reliable service largely depends on the efficient and uninterrupted operation of our computer network systems and data centers. Some of these systems have been outsourced to third-party providers. Any significant interruptions could severely harm our business and reputation and result in a loss of customers and large expenses to repair or replace the facility. Our systems and operations could be exposed to damage or interruption from power disruption, fire, flood, telecommunications failure, unauthorized entry and computer viruses, terrorism or other natural or man-made disasters. The steps we have taken and are taking to prevent a system failure, including backup disaster recovery systems,

may not be effective. Our property and business interruption insurance may not be adequate to compensate us for all losses or failures that may occur. Also, our third party insurance coverage will vary from time to time in both type and amount depending on availability, cost and our decisions with respect to risk retention.

Interest rates and credit ratings could adversely affect our cost of capital and net income.

Rising interest rates, credit market dislocations and decisions and actions by credit rating agencies can affect the availability and cost of our funding. Credit rating downgrades or negative changes to ratings outlooks can increase our cost of capital and hurt our competitive position. Guidance from rating agencies as to acceptable leverage can affect our returns as well.

We may suffer adverse financial consequences if Computer Sciences Corporation requires us to purchase its credit reporting business at a time when the public equity or debt markets or other financing conditions are unfavorable to us.

In 1988, we entered into an agreement with Computer Sciences Corporation, or CSC, and certain of its affiliates under which CSC’s credit reporting agencies utilize our computerized credit database services. Under this agreement, CSC has an option, exercisable at any time, to sell its credit reporting business to us. The option expires in August 2013. The option exercise price will be determined by an appraisal process and would be due in cash within 180 days after the exercise of the option. We estimate that if CSC were to exercise the option at December 31, 2010, the option price would have been approximately $625 million to $700 million. This estimate is based solely on our internal analysis of the value of

the business, current market conditions and other factors, all of which are subject to constant change. Therefore, the actual option exercise price could be materially higher or lower than the estimated amount. If CSC were to exercise its option, we would have to obtain additional sources of funding. We believe that this funding would be available from sources such as additional bank lines of credit and the issuance of public debt and/or equity. However, the availability and terms of any such capital financing would be subject to a number of factors, including credit or equity market conditions, general economic conditions and our financial performance and condition. Because we do not control the timing of the exercise, if any, by CSC of its option, we could be required to seek such financing and increase our debt levels at a time when market or other conditions are

unfavorable.

The acquisition, integration or divestiture of businesses by us may not produce the desired financial or operating results.

During 2010, we completed the acquisition of various businesses in separate transactions, including Anakam, Inc. and several international acquisitions, and divested our APPRO loan origination software and Direct Marketing Services businesses to align with our strategic focus. Expected benefits, synergies and growth from these initiatives may not materialize as planned. We may have difficulty assimilating new businesses and their products, services, technologies, and personnel into our operations. These difficulties could disrupt our ongoing business, distract our management and workforce, increase our expenses and materially adversely affect our operating results and financial condition. Also, we may not be able to

retain key management and other critical employees after an acquisition.

Our customers and we are subject to various current governmental regulations, and could be affected by new laws or regulations, compliance with which may cause us to incur significant expenses, and if we fail to maintain satisfactory compliance with certain regulations, we could be subject to civil or criminal penalties.

Our businesses are subject to various significant international, federal, state and local regulations, including but not limited to privacy and consumer data protection, health and safety, tax, labor and environmental regulations. These regulations are complex, change frequently and have tended to become more stringent over time. We may be required to incur significant expenses to comply with these regulations or to remedy violations of these regulations. Any failure by us to comply with applicable government regulations could also result in cessation of our operations or portions of our operations or impositions of fines and restrictions on our ability to carry on or expand our operations. In addition, because many

of our products are regulated or sold into regulated industries, we must comply with additional regulations in marketing our products.

Enactment of the Dodd-Frank Wall Street Reform and Consumer Protection Act and the rules and regulations that may be issued by U.S. regulators implementing such legislation (as well as actions that may be taken by legislatures and regulatory bodies in other countries) could limit our ability to pursue business opportunities we might otherwise consider engaging in, impose additional costs on us, result in significant loss of revenue, impact the value of assets we hold, or otherwise significantly adversely affect our businesses.

We also have agreements relating to the sale of our products to government entities, including through the Performance Assessment Network subsidiary of our TALX business and, as a result, we are subject to various statutes and regulations that apply to companies doing business with the government. The laws governing government contracts differ from the laws governing private contracts. For example, many government contracts contain pricing terms and conditions that are not applicable to private contracts. We are also subject to investigation for compliance with the regulations governing government contracts. A failure to comply with these regulations might result in suspension of these contracts, or administrative

penalties.

Third parties may claim that we are infringing their intellectual property and we could suffer significant litigation or licensing expenses or be prevented from selling products or services.

From time to time, third parties may claim that one or more of our products or services infringe their intellectual property rights. We analyze and take action in response to such claims on a case by case basis. Any dispute or litigation regarding patents or other intellectual property could be costly and time-consuming due to the complexity of our technology and the uncertainty of intellectual property litigation and could divert our management and key personnel from our business operations. A claim of intellectual property infringement could force us to enter into a costly or restrictive license agreement, which might not be available under acceptable terms or at all, or could subject us to significant damages or

to an injunction against development and sale of certain of our products or services. Our intellectual property portfolio may not be useful in asserting a counterclaim, or negotiating a license, in response to a claim of intellectual property infringement. In certain of our businesses we rely on third party intellectual property licenses and we cannot ensure that these licenses will be available to us in the future on favorable terms or at all.

Third parties may infringe our intellectual property and we may suffer competitive injury or expend significant resources enforcing our rights.

Our success increasingly depends on our proprietary technology. We rely on various intellectual property rights, including patents, copyrights, database rights, trademarks and trade secrets, as well as confidentiality provisions and licensing arrangements, to establish our proprietary rights. The extent to which such rights can be protected varies in different jurisdictions. If we do not enforce our intellectual property rights successfully our competitive position may suffer which could harm our operating results. Our pending patent applications, and our pending copyright and trademark registration applications, may not be allowed or competitors may challenge the validity or scope of our patents, copyrights or

trademarks. In addition, our patents, copyrights, trademarks and other intellectual property rights may not provide us a significant competitive advantage.

We may need to spend significant resources monitoring our intellectual property rights and we may or may not be able to detect infringement by third parties. Our competitive position may be harmed if we cannot detect infringement and enforce our intellectual property rights quickly or at all. In some circumstances, enforcement may not be available to us because an infringer has a dominant intellectual property position or for other business reasons. In addition, competitors might avoid infringement by designing around our intellectual property rights or by developing non-infringing competing technologies. Intellectual property rights and our ability to enforce them may be unavailable or limited in some countries

which could make it easier for competitors to capture market share and could result in lost revenue.

Economic, political and other risks associated with international sales and operations could adversely affect our results of operations.

Sales outside the U.S. make up approximately 27% of our net operating revenue and, as a result, our business is subject to various risks associated with doing business internationally. We anticipate that revenue from international operations will continue to represent an increasing portion of our total revenue. In addition, many of our employees, suppliers, job functions and facilities are increasingly located outside the U.S. Accordingly, our future results could be harmed by a variety of factors including changes in specific country or region political, economic or other conditions; trade protection measures; data privacy and consumer protection regulations; difficulty in staffing and managing widespread

operations; differing labor, intellectual property protection and technology standards and regulations; business licensing requirements or other requirements relating to making foreign direct investments, which could increase our cost of doing business in certain jurisdictions, prevent us from entering certain markets, increase our operating costs or lead to penalties or restrictions; difficulties associated with repatriating cash generated or held abroad in a tax-efficient manner; and geopolitical instability, including terrorism and war.

We earn revenue, pay expenses, own assets and incur liabilities in countries using currencies other than the U.S. dollar, including among others the British pound, the Canadian dollar, the Brazilian real, the Chilean peso and the Euro. Because our consolidated financial statements are presented in U.S. dollars, we must translate revenue, income and expenses, as well as assets and liabilities, into U.S. dollars at exchange rates in effect during or at the end of each reporting period. Therefore, increases or decreases in the value of the U.S. dollar against other major currencies will affect our net operating revenues, operating income and the value of balance sheet items denominated in foreign currencies. Because of